Annuity Lesson #22

How to Buy Annuities: A Complete Guide to Starting an Annuity

Jeremiah Konger

CEO

"An annuity may be particularly valuable for women who are concerned about outliving their money."

Retirement planning is no longer just for those approaching retirement age–it’s now a main priority for individuals of all ages. Many people are increasingly concerned about their savings and whether they will have enough to support a comfortable lifestyle in the future.

With an increasing number of people checking their nest eggs, knowing you can have a guaranteed income has become a sought-after viable option.

Diversifying investments is a smart strategy, and annuities have emerged as a popular option. With tax-deferred savings and a favorable interest rate, these financial products can help you achieve a stress-free retirement.

If you are looking for financial stability or low-risk investments, this guide is for you!

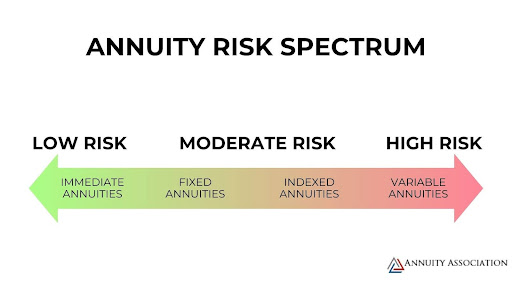

Understanding the Different Types of Annuities

An annuity is a long-term financial investment that offers the opportunity to maximize savings and provide you with a guaranteed income for life.

There are many types of annuities, but they can all be grouped into the following:

Provides a guaranteed interest rate and predictable payments, making it a low-risk option for steady retirement income.

- Fixed interest rate

- Guaranteed income

- Low risk

Variable Annuities

Offers investment in market-based options and returns that fluctuate based on market performance.

- Market-linked returns

- Higher growth potential

- Increased risk

Begins payouts almost immediately after a lump-sum investment, ideal for those needing instant income in retirement.

-

Payments start within a year

Deferred Annuities

Accumulates value over time, with payouts starting at a future date, offering tax-deferred growth and long-term income security.

-

Payments start at a due date

Many annuity providers offer another type that combines the benefits of fixed and variable products, known as fixed-indexed annuities or hybrid annuities. These products allow you to allocate a portion of your investments into market-based options like mutual funds and the rest to grow with a fixed interest rate.

Step-by-Step Guide to Buying an Annuity

The process of buying an annuity begins with thorough research. Our step-by-step guide walks you through how to start an annuity, from decision-making to finalizing your purchase.

Follow these instructions to ensure you're buying annuities that align with your financial goals and provide long-term benefits.

Step 1: Assess Your Financial Goals & Needs

First, you need to identify your needs to understand what annuity would best suit them. List the goals you want to achieve: protecting your money from inflation, receiving monthly payments during retirement, or growing your money in a low/high-risk environment.

Another factor to consider is your current income. You can evaluate whether your cash flow will be enough or whether you would like to establish an additional income.

Lastly, you should choose between fixed and variable annuities–or go for a hybrid offer. While fixed annuities offer some protection, ensuring steady income with investment losses, variable annuities provide a greater chance to maximize your savings but at a higher risk.

Question to Ask Yourself

- How much guaranteed income will I need in retirement to cover essential expenses?

- Am I comfortable with market risk, or do I prefer a stable, predictable income?

- How much are my monthly expenses?

Step 2: Choose the Right Type of Annuity

It may be difficult to find the right type of annuity for your financial needs. To ease your search, you should consider the following factors:

- Growth potential: Each annuity comes with its own growth opportunity, including fixed or index-based rates. When choosing an annuity product, pay extra attention to how much it can grow your savings and whether the outcome aligns with your financial goals.

- Risk tolerance: Before buying an annuity, never skip a risk check. Lower-risk annuities with a fixed rate provide smaller yet consistent growth, and higher-risk variable annuities offer a better growth opportunity with possible market fluctuations. The choice is yours.

- Payout flexibility: Annuity payouts come in different forms: lump-sum, immediate, lifetime, and period or monthly. Choose the one that will provide you with an income you will be comfortable with.

We have selected the most popular financial goals of our clients and what annuities were recommended to them:

| Financial Goal | Most Suitable Annuity Type | Reason |

| Guaranteed lifetime income | Immediate Annuity, Deferred Annuity | Provides predictable, guaranteed income for life or a set period. |

| Growth before retirement | Deferred Annuity, Fixed Index Annuity | Allows funds to accumulate with potential for growth before income payouts begin. |

| Market participation with downside protection | Fixed Index Annuity | Offers market-linked growth with protection against losses. |

| Higher growth potential with investment flexibility | Variable Annuity | Direct market participation with higher growth potential but greater risk. |

| Maximizing income later in retirement | Deferred Annuity | Provides a future income stream with built-in growth to maximize payouts. |

| Protecting against outliving savings | Immediate Annuity, Deferred Annuity | Ensures a reliable income stream that cannot be outlived. |

| Balancing growth and security | Fixed Index Annuity | Offers market-linked returns with varying degrees of downside protection. |

Step 3: Compare Annuity Providers

After choosing the type of annuity that best meets your expectations, you should search for a reliable provider.

During our consultations, we often recommend companies that meet the following criteria:

- Positive reputation

- Good customer support

- Favorable contract terms

- High ratings (including AM Best, S&P ratings, and Moody’s score)

Save yourself a ton of time searching for annuity products through the web and take our intuitive Annuity Quiz–see what financial product is right for you in a few clicks.

Step 4: Understand Fees, Costs, and Payout

Each annuity comes with certain fees you should be aware of. While your investment is growing, you may have to cover expenses associated with your contract.

Here is a breakdown of common annuity fees:

- Annuity premium: This is your initial investment in the annuity of your choice. It is typically paid as a lump sum (usually a minimum of $10,000) or as monthly payments.

- Annuity commission: If applicable, you may need to pay agents a percentage of your contract value when you sell your annuity. These commissions are often included in the total price.

- Administrative fees: A small yearly fee that is paid to cover the maintenance and management of your contract.

- Surrender charges: If your withdrawal exceeds the allowed amount, you will have to pay a surrender charge, which is typically 10% of your annuity value.

- Mortality and expense fees: A small annual fee that serves as compensation to the insurer for covering risk.

- Investment expense ratio (only applicable to variable annuities): A small annual fee that is paid to cover fund management and investment costs.

- Riders fees: You can opt for additional riders for an extra charge. These include death benefits, guaranteed minimum withdrawal benefits, etc.

Wondering what fees may apply to your type of annuity? Check out our comparison table below:

| Annuity Type | Administrative fees | Surrender charges | Mortality and expense | Investment expense ratio | Riders (optional) |

| Fixed | 🟡 | ✅ | ❌ | ❌ | 🟡 |

| Variable | 🟡 | ✅ | ✅ | ✅ | ✅ |

| Fixed Indexed | 🟡 | ✅ | 🟡 | ❌ | ✅ |

| Immediate | 🟡 | ❌ | ❌ | ❌ | 🟡 |

| Deferred | 🟡 | ✅ | ❌ | ❌ | 🟡 |

✅- Yes, ❌- Not, 🟡- Sometimes included

Step 5: Compare Annuity Payout Options

By now, you’ve probably noticed that annuities are flexible financial products that you may customize to suit your financial needs. One element of this personalization is choosing your preferred payout option.

Depending on the provider and company, your annuity contract may already have a pre-defined payout option.

Here are possible payout options:

- Life-only annuity: Provides the highest payout, but payments stop at death, with no benefits for heirs.

- Joint-and-survivor annuity: Lower payout than life-only but ensures payments continue to a spouse after your passing.

- Fixed amount (systematic withdrawals): You choose a fixed monthly amount, but there's no guarantee you won’t outlive your funds.

- Fixed period (period certain): Payments are guaranteed for a set period (e.g., 10, 15, or 20 years). If you pass away early, beneficiaries receive the remaining payments.

- Life with period certain: Guarantees payments for life but also includes a minimum payout period, ensuring your beneficiaries can receive remaining funds if you pass away early.

- Lump sum payment: A one-time payout of your entire annuity. This option comes with significant tax implications.

Not sure which payout option would be best for you? Check the comparison table below:

| Payout Options | For Life | Beneficiary | Stops at Death | Certain Period |

| Life-Only | ✅ | ❌ | ✅ | ❌ |

| Joint-and-Survivor | ✅ | ✅ | ❌ | ❌ |

| Fixed Amount (Systematic) | ❌ | ❌ | ✅ | ❌ |

| Fixed Period (Period Certain) | ❌ | ✅ | ✅ | ✅ |

| Life with Period Certain | ✅ | ✅ | ❌ | ✅ |

| Lump Sum Payment | ❌ | ❌ | ❌ | ❌ |

Step 6: Decide When to Buy an Annuity

Any adult can buy an annuity, but statistics show that younger individuals often don’t prioritize them. Annuities typically become a more attractive option starting around age 50, when the need for additional income and investment diversification grows.

For those in their 60s who are nearing retirement, annuities can help protect against the risk of inflation and provide a reliable income stream before retirement begins.

Many financial advisors recommend purchasing an annuity at age 70 or older, as it can supplement Social Security benefits and create an additional income source to cover long-term care costs.

Step 7: Work with a Licensed Annuity Expert

The final and most important step is choosing how to purchase an annuity: directly from a provider or with a financial advisor. One option has certainly more advantages than the other:

Annuity Provider

When purchasing directly from a provider, the annuity would be sold through one of the company’s agents.

The downside here is that these agents receive a provision from the product they have access to.

This means there is a high chance you will not be presented with better alternatives.

Financial Advisor

In comparison, independent agents work with multiple annuity providers and have access to a broader range of products.

These agents provide the same level of assistance but can present more options.

This means you can find the financial product that aligns perfectly with your financial goals.

Frequently Asked Questions (FAQs) About Buying Annuities

How much do you need to start an annuity?

Minimums vary by type—typically $10,000-$25,000 for a lump sum or $2,500–$5,000 for installment payments.

Are annuity payments taxable?

Yes, taxes apply to earnings when withdrawn. Qualified annuities are taxed as ordinary income, while non-qualified annuities are taxed on the growth portion only.

Can I withdraw money early?

Yes, but early withdrawals (before 59½) may incur a 10% IRS penalty plus surrender charges.

What happens to my annuity after I pass away?

It depends on the contract. Some annuities offer a death benefit for beneficiaries, while others stop payments upon your passing.

Final Thoughts & Next Steps

Annuities can be a valuable retirement strategy that will provide a guaranteed income for life and also protect your loved ones after your passing. But before purchasing annuities, you should carefully compare the product offers, their fees, and payout options.

Only when you’re confident about your choice should you sign an annuity contract.

If you are unsure what annuity products are available that can maximize your savings, consult with one of our financial advisors.

Annuity Expert

Jeremiah Konger

PS - Here's 3 ways we can help you learn more about annuities.

1. Watch Videos on How to Identify The Highest Paying Protected Income & Growth Annuities.

2. Watch Videos That Reveal What to Look For When Buying A Protected Growth Annuity.

3. Click Here To Access Our Annuity Review Vault To Compare The Pro's and Con's of Dozens of Annuities.

-

Serving All 50 States

-

info@annuityassociation.com

-

855-866-3659

ABOUT US

Annuity Association is the leader in providing Independent Annuity recommendations for protected income, safe growth and other benefits in retirement.

© Copyrights by Annuity Association. All Rights Reseved.