Annuity Lesson #22

Fixed vs. Fixed Index vs. Variable Annuities

Jeremiah Konger

CEO

"An annuity may be particularly valuable for women who are concerned about outliving their money."

When choosing a long-term investment, many people have to choose among a multitude of products that each offer their unique benefits. But when it comes to an investment that can provide a steady stream of income – annuities are often a popular choice, especially for retirement.

Annuities come in several forms, each with its own benefits, risks, and growth potential. Hence, it is crucial to understand the differences between fixed annuities, fixed index annuities, and variable annuities and choose the one that matches your goals.

In this guide, we’ll break down each type of annuity, highlight its pros and cons, and help you compare features so you can make informed decisions.

If you've ever wondered things like “How does an indexed annuity differ from a fixed annuity?” or whether a variable annuity is worth the risk – you will find your answers below.

Key Takeaways

- Fixed annuities offer guaranteed interest and low risk, while fixed index annuities provide moderate growth potential by linking returns to a market index with downside protection.

- Variable annuities invest in market-based sub-accounts, offering higher growth potential but with greater risk, fees, and complexity.

- Choosing the right annuity depends on your risk tolerance, income needs, and long-term financial goals—consulting a financial advisor is key for a tailored strategy.

What Is a Fixed Annuity?

A fixed annuity is an insurance contract that guarantees a fixed interest rate on contributions made by the annuitant. In exchange for a lump sum or a series of premium payments, the insurance company promises to pay a guaranteed income, either immediately or at some point in the future.

This is a good investment choice for conservative investors who prioritize gradual growth with low-risk levels and retirees who want predictable outcomes.

Fixed annuities typically offer guaranteed returns ranging from 3% to 6%.

How Fixed Annuities Work

Fixed annuities grow at a pre-determined interest rate, unaffected by stock market fluctuations. That predictability makes them a conservative and secure choice for individuals who prioritize stability over growth potential. They’re especially popular among retirees who want consistent monthly income without risk.

When investing in a fixed annuity, you will know what interest rate you will benefit from and then receive your savings for a set number of years or for your life.

Fixed annuities can be divided into two main phases:

- Accumulation phase – Your money grows at a fixed interest rate.

- Payout phase – The insurer provides income payments, often for life.

Pros and Cons of Fixed Annuities

Fixed annuities are often considered a secure and predictable investment, but they also come with their downsides:

Real Life Example

-

Investor: Jane

-

Age: 60

-

Type of Investor: Conservative Investor

Jane was looking for peace of mind and a predictable retirement income. She wanted to have a guaranteed income that would help you cover the cost of everyday living. That’s why Jane invested in a fixed annuity with a 3.5% annual rate. Her principal is protected, and she has received a steady income for 15 years.

What Is a Fixed Index Annuity?

A fixed index annuity (FIA) is a hybrid product that combines the safety of a fixed annuity with the potential for higher returns linked to a stock market index, such as the S&P 500.

When comparing indexed annuity vs. fixed annuity, we can clearly see that this product protects against market losses while offering growth potential linked to stock market indexes. Hence, fixed-indexed annuities offer an appealing middle ground for conservative investors who still want some upside potential.

How Fixed Index Annuities Work

The interest credited to your account is based on the performance of a selected index, but it does not directly invest in the market. Instead, the insurer uses a crediting formula that may include:

-

Participation rate (e.g., 80% of the index gain)

-

Cap rate (e.g., max gain of 6%)

-

Floor (e.g., 0%—you won’t lose money due to market downturns)

So, how does an indexed annuity differ from a fixed annuity? While both offer principal protection, indexed annuities allow you to earn more based on market performance—without risking your initial investment.

At the same time, unlike variable annuities, which highly depend on the market performance, fixed-indexed annuities offer some protection against big losses.

Pros and Cons of Fixed Index Annuities

Even though a fixed-indexed annuity offers a balanced growth opportunity – there are a few disadvantages to take into account:

Real Life Example

-

Investor: Mike

-

Age: 55

-

Type of Investor: Balanced Risk

Mike is five years from retirement and doesn’t want to lose money but wants better returns than a CD. He chooses a fixed index annuity tied to the S&P 500. One year, the index rises 8%, but due to a cap of 6%, he earns 6%. When the market drops the next year, his return is 0%, not negative—his principal stays intact. Although it becomes hard to calculate how much he can maximize his earnings – Mike knows that he’s taking advantage of the positive market performance.

What Is a Variable Annuity?

A variable annuity offers investment options similar to mutual funds (called sub-accounts), where your returns are tied directly to the performance of those investments. While this comes with greater growth potential, it also involves higher risk, including the possibility of losing principal.

With a variable annuity, you invest directly in market-based funds (e.g., stock, bond, real estate, and other types of funds). Unlike fixed-indexed annuities, this investment product doesn’t place a cap rate on your earnings but also lacks any sort of protection against market losses.

How Variable Annuities Work

You choose from a menu of sub-accounts. Your money is invested, and its value fluctuates with the market. In the payout phase, your income can vary based on how your investments have performed—though some annuities offer optional riders for guaranteed income.

By now, you may be less willing to invest in variable annuities – however, keep in mind that your provider can help you tailor your annuity by investing in conservative or aggressive funds (or a combination of both). Hence, the risk level will depend on the market indexes of your choice.

Pros and Cons of Variable Annuities

Variable annuities aren’t ideal – they are riskier compared to other types of annuities and more sophisticated. However, savvy investors choose this investment for the following benefits:

Real Life Example

-

Investor: Lisa

-

Age: 50

-

Type of Investor: Growth Seeker

Lisa invests in a variable annuity with aggressive sub-accounts. She knows the risks and opportunities of your investment. Over 10 years, her portfolio has grown significantly, though she experiences volatility. She adds an income rider to guarantee withdrawals regardless of market performance and makes her variable annuity more secure than it was before.

Comparing Fixed, Fixed Index, and Variable Annuities

The best way to compare fixed annuity vs. fixed-index annuity vs. variable annuity is to put them side-by-side. Let’s break down the key differences between these three types in the categories that matter most to retirees and investors.

Interest Rates and Growth Potential

When it comes to interest rates and growth potential, each annuity offers something different yet suitable for investors of any type:

From the comparison table, you can immediately see that:

-

Fixed annuities guarantee a steady but modest return. It isn’t a product with the best growth potential but it offers security that many investors look for.

-

Fixed index annuities offer a blend of security and growth. They are a popular choice for their opportunity to maximize savings without taking a hit for market downturns.

Finally, variable annuities offer the highest upside—but also carry the most risk. If you are experienced in investing or have a proficient annuity advisor, you can rely on the expertise and tailor the annuity to match your preferred risk level.

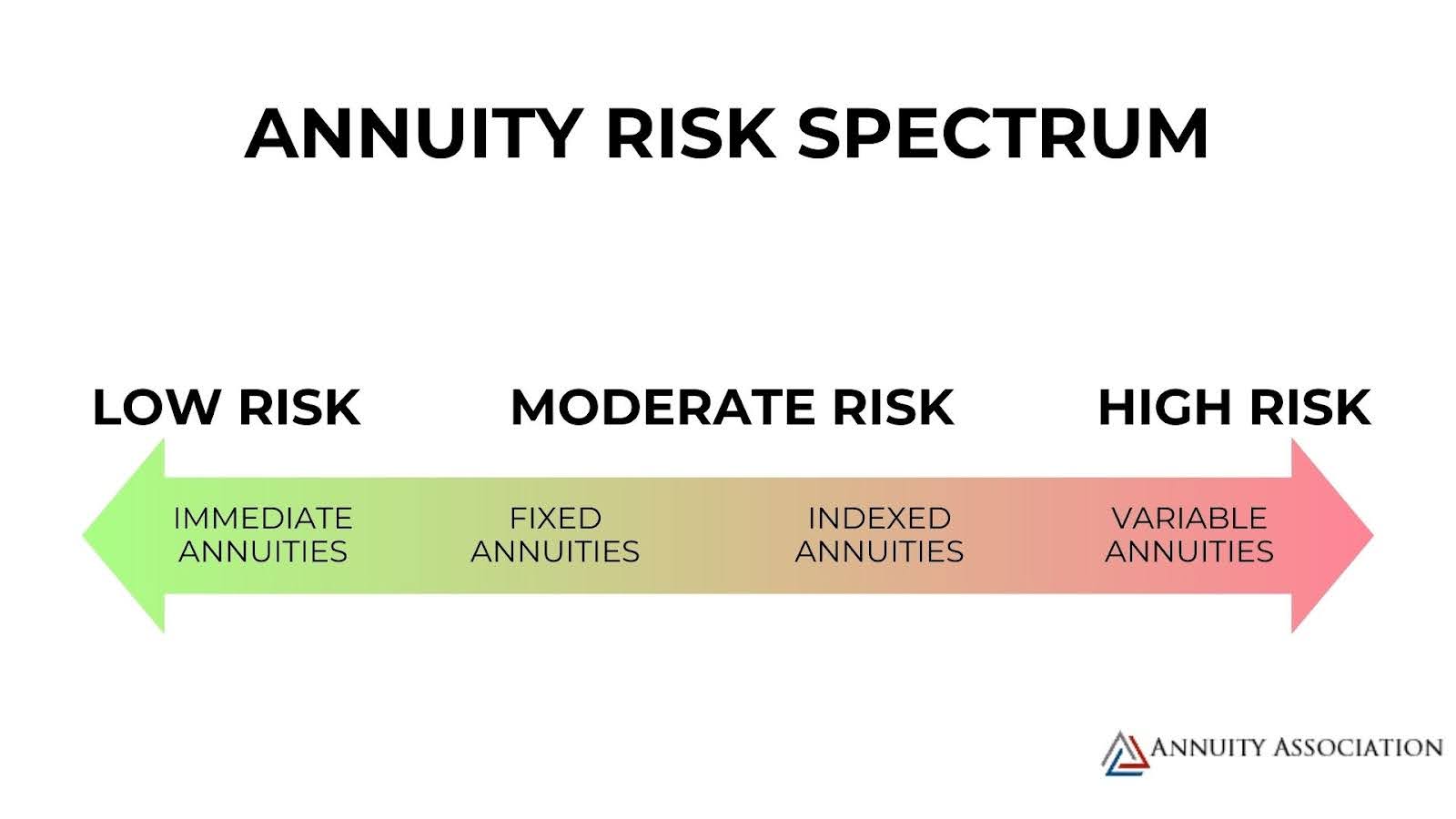

Risk Levels

Many investors and retirees choose annuities by their risk level. It’s no secret that fixed annuities are considered the safest investment, but how do they compare to other annuity types:

What we can conclude from this comparison is that:

-

Fixed annuities suit risk-averse investors and retirees who seek peace of mind that their savings will benefit from a set interest rate.

-

Indexed annuities work best for those wanting some market exposure with downside protection. This means you can get the most out of your annuity while not losing money in the case when market indexes underperform.

-

Variable annuities are best for growth-oriented investors comfortable with market fluctuations and those who understand the risks associated with this investment. We recommend them for those with previous investment experience.

Fees and Expenses

Most annuities include administrative fees in the contract price, but some will have this note written in small print. Hence, you should know what extra costs you may have to pay after investing in an annuity.

Here are common annuity fees:

-

Annuity premium: Your initial investment is either a series of payments or a sum of money.

-

Annuity commission: Often included in the percentage of your contract value, it is a fee for an agent.

-

Administrative fees: A yearly fee paid for annuity maintenance.

-

Surrender charges: When withdrawing over a permitted amount from the contract, you will have to pay a fee, typically 10% of your annuity value.

-

Mortality and expense fees: A fee you pay yearly as compensation to the insurer for covering risk.

-

Investment expense ratio: A fee that covers the management of an annuity.

-

Riders: Additional fees for add-ons like death benefits, guaranteed minimum withdrawal, etc.

See what annuity types may include extra fees:

✅- Yes, ❌- Not, 🟡- Sometimes included

Among all annuities, fixed ones have the lowest fees, while variable products come with the highest extra costs for admin fees, management fees, and other. Fixed index annuities may include costs for riders or indexing formulas.

Liquidity and Surrender Charges

Most annuities come with surrender periods, often ranging from 5 to 10 years, during which early withdrawals incur penalties. However, many offer free withdrawal allowances (e.g., 10% annually).

Variable annuities may also have market value adjustments or withdrawal fees based on investment performance.

Tax Considerations

Contributions grow tax-deferred in all annuity types. You will only need to pay taxes if you decide to have an immediate payout.

⚠️ Keep in mind that withdrawals are taxed as ordinary income, not capital gains. Plus, if you withdraw before age 59½, you may incur a 10% IRS penalty.

How to Choose the Right Annuity for Your Financial Goals

Choosing the right annuity depends on your personal financial situation, investment goals, and risk tolerance. While all annuities offer their pros and cons, knowing the steps to how to choose the right investment to match your financial goals is important:

1. Assess Your Risk Tolerance

Ask yourself what your financial goals and needs are, whether your current income is enough, and whether risky investments are something you can tolerate.

If you prefer guaranteed income and stability, you should consider a fixed annuity may suit you best.

If moderate-risk investments with upside potential are what you’re looking for, then fixed-indexed annuities may be the right investment for you.

Finally, if market risks do not scare you and you seek growth of your savings, variable annuities may help maximize your savings.

2. Define Your Financial Goals

To understand your goals, you should ask yourself:

-

Do I need a lifetime income?

-

Am I seeking tax-deferred growth?

-

Am I comfortable with market fluctuations?

Depending on your answers, you can opt for the following annuities:

-

A fixed annuity offers a set interest rate and acts as a bond substitute, offering an additional source of income.

-

A fixed-indexed annuity can be the investment that balances your portfolio, offering growth potential and protection from low market performance.

-

Variable annuities may serve long-term growth goals depending on the market indexes you choose.

3. Understand the Product

Before signing an annuity contract, how can you be certain your investment won’t end up costing more than what’s advertised in the marketing brochure? To protect yourself, make sure you fully understand the details of the annuity by reviewing the following:

-

Contract terms

-

Fees and charges

-

Indexing strategies

-

Surrender periods

Annuities can be complex, and small details can impact your returns and liquidity.

4. Consult a Financial Advisor

The most effective way to match the right annuity to your goals is by speaking with a licensed financial advisor. They can help clarify whether you need a guaranteed income, growth, or a blend of both, and show how different annuities fit into your overall retirement plan.

At Annuity Association, we’ve helped numerous people find suitable investment opportunities to maximize their savings and ensure a guaranteed income for life.

Conclusion

Deciding between a fixed annuity, fixed index annuity, or variable annuity ultimately depends on your financial goals, risk tolerance, and desired level of flexibility. Each type offers unique advantages, but they also carry different levels of risk.

Understanding the features and trade-offs of each option will help you make a more informed and confident decision. Here is a short summary of each annuity mentioned in our guide:

-

Fixed annuities offer guaranteed income and principal protection.

-

Fixed index annuities provide a balance of growth and security.

-

Variable annuities deliver growth potential but with higher risk and fees.

Now that you know the differences, we hope you’ll be better equipped to build a retirement strategy that provides lasting income and peace of mind.

Annuity Expert

Jeremiah Konger

PS - Here's 3 ways we can help you learn more about annuities.

1. Watch Videos on How to Identify The Highest Paying Protected Income & Growth Annuities.

2. Watch Videos That Reveal What to Look For When Buying A Protected Growth Annuity.

3. Click Here To Access Our Annuity Review Vault To Compare The Pro's and Con's of Dozens of Annuities.

Annuity Association is the leader in providing Independent Annuity recommendations for protected income, safe growth and other benefits in retirement.

-

Serving All 50 States

-

-

Annuity Association

759 SW Federal Hwy Ste 200H

Stuart, FL 34994

© Copyrights 2025 by Annuity Association. All Rights Reseved.